Make the IRS Your Last Beneficiary - Not Your Biggest One!

For Texas Couples with $250,000 + in Qualified Assets such as 401(k)s, IRAs, and 403 (b)s

Discover how smart Texas retirees are protecting principal, eliminating future tax surprises, avoiding out-of-pocket conversion taxes, and creating future tax-free income using our proven Roth Conversion Strategy.

Why Retirees Are Acting Now

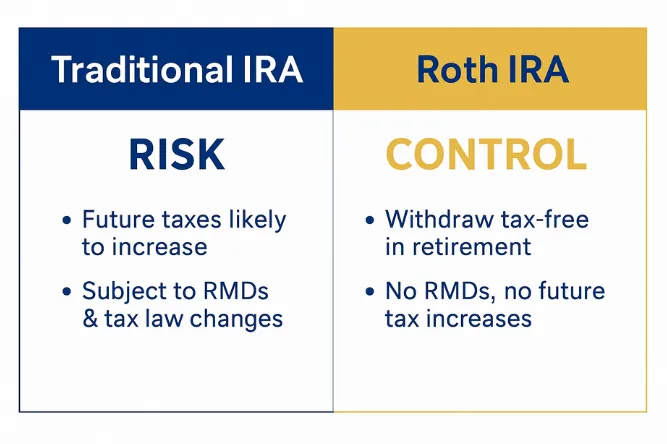

Every dollar withdrawn from your IRA/401(k)/403(b) is taxable. When today's lower rates sunset, retirees could pay significantly more to the IRS. There is a way to lock in current low marginal rates and convert safely - without paying the taxes out of your pocket.

Avoid surprise tax bills in retirement

Avoid higher tax brackets later in retirement

Protect your principal from market volatility and downturns

Eliminate future required minimum distributions (RMD's)

Protect your heirs from potential legacy tax burden

Create a predictable future tax-free income stream

Every year you wait, more of your retirement becomes taxable forever

Every year you wait, the IRS becomes your biggest beneficiary (and you or your heirs keep less).

This is why most retirees overpay the IRS - Unintentionally

The Smart Roth Conversion Strategy Trusted by North Texas Retirees

Our approach helps you convert portions of your savings to tax-free income while using tax efficient funding so you don't have to pay the taxes out-of-pocket. Your principal stays protected!

Step 1: Analyze

We identify your tax bracket, conversion window, and ideal amount to convert each year — without paying taxes out of pocket.

Step 2: Implement

We help you reposition a portion of your IRA using strategies designed to minimize taxes and reduce future RMDs.

Step 3: Enjoy

You receive tax-free income in retirement and peace of mind knowing the IRS cannot increase taxes on converted funds.

See How Much Tax-Free Income You Could Create - In Under 2 Minutes

You’ll instantly learn whether a Roth Conversion could save you thousands in future taxes.

Takes less than 2 minutes. No Pressure. No obligation.

Featured on Safe Retirement Radio

Licensed Fiduciary I Independent Advisor I Since 1993

Meet Guy McCord

Trusted by 1000+ Texas Families Since 1993

Guy McCord is a Texas-based Independent Advisor specializing in Tax-Free Income Strategies, Roth Conversions, and Retirement Planning for individuals ages 55–75+. For over 30 years, he has helped retirees reduce taxes, avoid market risk, and protect their lifetime income.

Why Guy's Clients Choose Him:

Based in Texas - understands local planning needs

Over 30 Years of Experience

Fiduciary approach to your plan since 1993

Expert in tax-free income strategies and risk elimination

Insurance backed guarantees

“Our mission is simple...help you keep more of what you have earned by aligning your plan with today's tax reality."

- Guy McCord, Licensed Fiduciary since 1993

Real Texans. Real Results. Real Tax Savings.

"We finally understood our 401k/IRA tax exposure and it was alarming. Guy helped put a plan together to reduce it.

- John and Nancy T., Houston, TX

⭐⭐⭐⭐⭐

"Guy's approach made things very simple. He is no fluff and direct. We are converting our IRA's in stages while keeping our principal in tact."

- Michele and Mark M. - Tomball, TX

⭐⭐⭐⭐⭐

"Clear, non-salesy approach. I feel confident about our retirement income now after working with Guy."

- Linda H. - San Antonio, TX

⭐⭐⭐⭐⭐

“Guy ran our Roth Conversion analysis and helped us convert over five years without paying anything out of pocket. We now have predictable tax-free income for life and are protected from market risk.”

— Jim & Kathy, Beeville, TX

⭐⭐⭐⭐⭐

You're Not the Only One Asking Questions...

💡Will converting affect my Social Security or Medicare Taxes?

Because a Roth conversion increases your adjusted gross income (AGI), it can push you into higher provisional income ranges, meaning a greater portion of your Social Security benefits becomes taxable that year. Medicare Part B and Part D premiums are means-tested, based on your Modified Adjusted Gross Income (MAGI) from two years prior. If your Roth conversion causes your MAGI to exceed those thresholds, your Medicare premiums can increase by hundreds per month per person for the next year.

Those tax and Medicare effects are temporary — the conversion is taxed once, but future Roth IRA withdrawals are:

-Tax-free

-Do not count toward AGI

-Do not affect Social Security taxation

-Do not trigger higher Medicare premiums

So while a conversion may raise taxes and IRMAA in the short term, it can reduce future taxable income — keeping your Social Security benefits and Medicare premiums lower throughout retirement.

💡Is there any cost or obligation?

No. Your initial session is completely complimentary and designed to provide education — not a sales pitch. You’ll receive a personalized Roth conversion roadmap you can use whether you work with us or not.

💡Will I owe taxes immediately after converting?

Yes, conversions are taxable — but our strategy pays the tax due and helps minimize or offset those taxes using current deductions, smart timing, and other planning tools. Many clients are surprised how affordable it can be when structured correctly.

💡Can I still do this if I’m already retired?

Absolutely. In fact, many retirees are in their lowest lifetime tax bracket during early retirement — which makes it one of the best times to convert to a Roth and lock in tax-free growth for the rest of your life.

💡What if I already did a partial Roth Conversion before?

You can still convert additional amounts. In fact, many families benefit most when conversions are done in phases. Your personalized strategy will show the ideal conversion amount per year.

💡Does a Roth Conversion trigger an audit?

No. But many people think it does.

Take Control of Your Retirement- Let's Make Your Future Income Tax-Free

Every year you wait, your retirement taxes increase. See your numbers today.

Prefer to talk now? Call us directly at 972-449-4446

Guy McCord with Spaam Enterptises Inc specializes in arming clients with knowledge and awareness about their money

that empowers them to make better financial decisions for their family and their future.

The information being provided is a courtesy. When you click on any link to another website provided herewith, you are leaving this site.

Spaam Enterprises Inc makes no representation as to the completeness or accuracy of information provided at these sites. Nor is the company liable for any direct or indirect technical or system issues or any consequences arising out of your access to or your use of third-party technologies, sites, information and programs made available through this site. When you access one of these sites, you are leaving the Guy McCord website and assume total responsibility and risk for your use of these sites.

Information regarding securities issues and markets is obtained from sources believed to be reliable, but is not guaranteed as to accuracy, completeness, or fitness to a particular use. This website is intended solely to convey general information about the products and services provided by Guy McCord and is not investment advice or the solicitation for the purchase or sale of any product or service.

Licensed in TX I Fiduciary Advisor

Copyright 2025 | Guy McCord | Privacy Policy